It’s Blue Cross Blue Shield All The Way Down: What is Public Insurance, and How Much Does It Matter?

Public insurance. The ideal method for most single payer advocates and progressives across the US, and the enemy of the conservatively minded. To some, the only way forward to establish true quality care. To others, enemy number one in the fight over government overreach. And to some others, yet another option to ensure a functional competitive market.

Public insurance and public health care are typically cited in the United States as Medicaid (the program for the needy), Medicare (the program for the elderly and disabled), the Veterans Health Administration (the socialized medical system for military families), and the Indian Health Services. This contrasts with employer insurance, individual Affordable Care Act (ACA) marketplace also known as Obamacare, and off-market plans. But what makes a program public versus private?

Most people would say an insurance program becomes public when it is funded and run by the government. Public insurance doesn’t even require public providers, nor does it mean that the care must be free at point of service. Care can be delivered by for-profit providers for a fee, as long as the government is the insurer, and enrollees can be required to share some of the burden. In fact, most countries in the developed world have significant per capita out of pocket costs each year. Some using “private” insurance, some “public” insurance, and mostly a mix. But do the United States’ public insurance programs meet this definition?

Medicaid and Managed Care Organizations

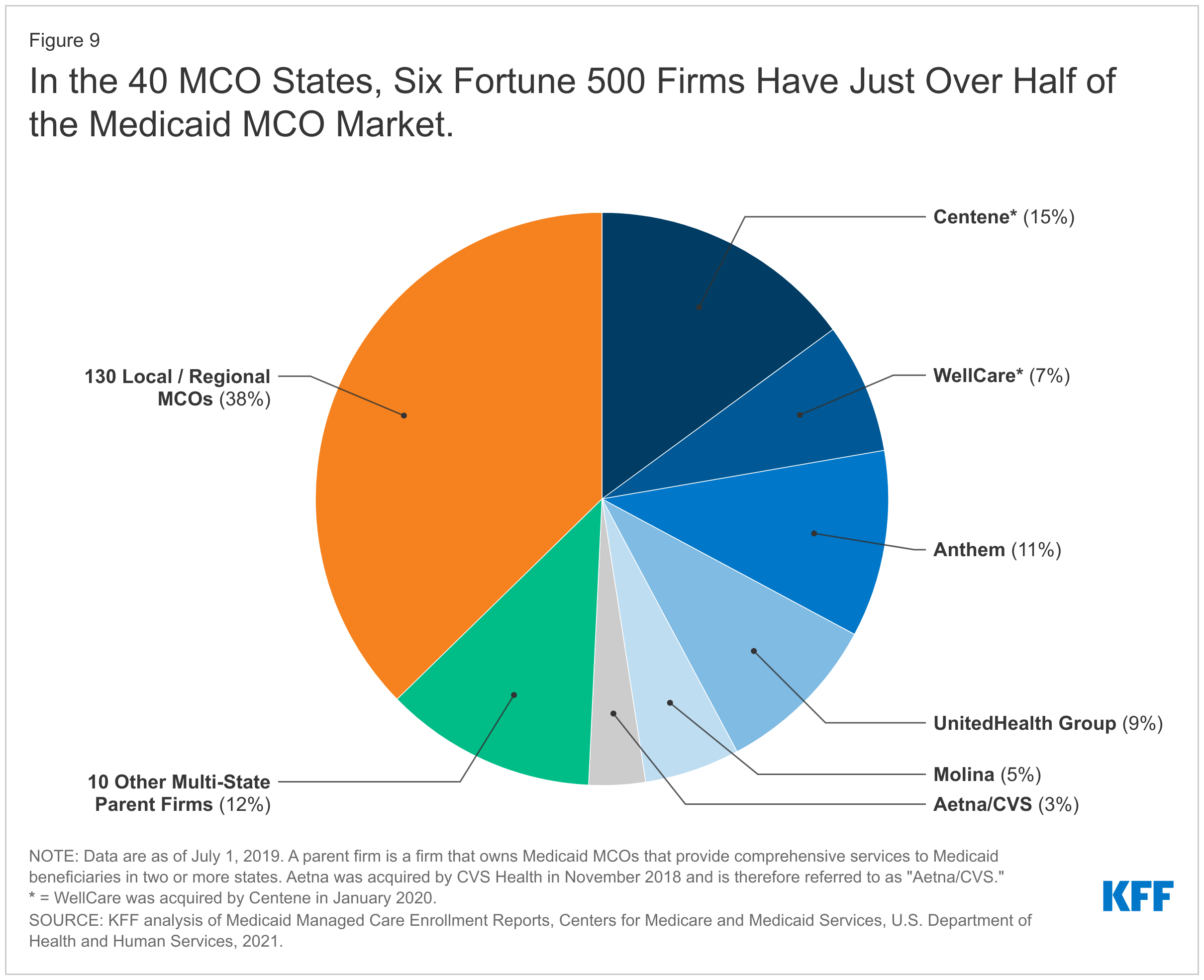

Let’s start with Medicaid, the program for the needy. In July 2020, 72% of all enrollees were managed by private companies via Managed Care Organizations (MCOs) that managed the needs of a state’s Medicaid population using fixed monthly payments per enrollee, called capitation. Some estimates put the MCO share at as high as 90% according to Charles Gaba at ACAsignups.net. These amounts are adjusted and paid out via population risk scores from the state government to the MCO, using the pool of money states have allocated along with the Federal government’s matching share. In fact, 41 states and DC contract with Medicaid MCOs, and 25 states have more than 75% of their enrollees covered in these organizations. These organizations then form networks of private providers just like private insurance does. In those few remaining states and for other enrollees not covered by Medicaid MCOs, government-run programs are used for coverage. In terms of dollars, Medicaid MCOs accounted for just over half of all Medicaid spending. And a handful of firms service the majority of MCOs: Centene at 15%, Wellcare (owned by Centene) at 7%, Anthem (affiliated with Blue Cross Blue Shield) at 11%, UnitedHealth Group at 9%, Molina at 5%, and Aetna/CVS at 3%.

Medicare, Prescription Drug Plans, Supplemental Plans, and Medicare Advantage

Then there’s Medicare, the program for the elderly and disabled. This program has been split into four major parts: Parts A, B, C, and D. Parts A and B are the traditional hospital and medical insurance people receive at the national level with premiums for Part B, and separate copays, coinsurance, and deductibles. These are what is considered proper government run insurance, though technically the payment systems are managed by Medicare Administrative Contractors since 2003. Part D is a voluntary program that uses a publicly subsidized private marketplace for prescription drug coverage with many of the same companies you will find with employer plans. About 9 in 10 Medicare enrollees with traditional Medicare purchase these plans, and many also purchase supplemental private Medigap plans or have employer retirement supplemental benefits. That’s all before considering Medicare Part C, or Medicare Advantage. This is a private, often for-profit, alternative to Medicare Parts A and B (with voluntary drug coverage in an Advantage plan in place of Part D) that allows for other benefits and an out-of-pocket maximum in a single bundle. Like Medicaid MCOs, Medicare Advantage and Medicare Part D are adjusted using risk scores (along with quality targets for at least Medicare Advantage) and the government pays these private companies a per enrollee per month fee; the same capitated model, just a different budget. About half of enrollees are in Medicare Advantage, and the CBO projects they will overtake traditional government Medicare very soon. At present, there is no reason to believe this trend will reverse course.

The companies that compete for enrollees in these plans? They are very similar to Medicaid MCOs, with UnitedHealthcare alone accounting for more than a quarter of all enrollees.

Obamacare and Employer Insurance

What about employer coverage and the individual marketplace? Rather than being government run plans or private capitated plans, Obamacare plans issue no requirements on reimbursement rates or total expenditures and allow private insurers to negotiate with providers, just like employer plans. And just like employer plans, insurers must guarantee issue regardless of health status and must charge everyone the same premium. The big difference comes from the age band, where enrollees in the individual market can have their premiums based on their age with people aged 64 charged about three times what people around age 21 are charged. Insurers must spend 80% of revenue on medical care, and markets are risk-adjusted so that insurers with a healthier pool must compensate insurers with a sicker pool. Premiums are still quite expensive, so the federal government will compensate enrollees for their premiums via fully refundable tax credits that scale by income and can be paid out per month or in lump sum, called Advanced Premium Tax Credits. The government will also aid with out-of-pocket costs by setting Cost Sharing Reduction (CSR) requirements when insurers cover people that make less than 250% of the poverty rate. Expenses paid at point of service are set with “metal levels” where the insurer is expected to cover 60%-90% of their enrollee population’s expenses from their premium revenue, while in Medicaid Managed Care there are small copays and insurers are expected to manage expenses using their monthly payment from the government.

As an alternative to Obamacare, the states can also create Basic Health Plans for people that make less than 200% poverty. Only New York and Minnesota use this so far, and New York uses them for potential Obamacare CSR enrollees and immigrants ineligible for Medicaid. However, these are managed by private insurers as well.

In employer markets, employees are all charged the same premium, but they have a much smaller risk pool than many of these public set ups where risk pools could be national or regional. Government subsidy comes through the back end with these plans by exempting them from federal taxes. And regulation comes from federal regulation via ERISA.

According to the American Medical Association, you’ll again see the major insurers of Blue Cross Blue Shield, UnitedHealthcare, Aetna/CVS, Cigna, Humana, and more.

State “Public” Options

Within these state exchanges, so called “public options” are finally being created. As you may recall, the debate for the ACA featured a contentious discussion on the inclusion of a public option in the individual marketplace to hold down insurer prices via competition. This was removed to prevent Senator Joe Lieberman joining Republicans in a filibuster that would destroy any remaining hope for comprehensive healthcare reform. More than a decade after the ACA was passed, Washington, Nevada, and Colorado are finally acted to pass their own “public options” to hold down consumer premiums and increase competition. More states are likely to follow over time. Are these plans managed by the government like the small minority of Medicaid plans and less than half of Medicare? No. In all cases, these “public options” are private Obamacare plans that are slightly more regulated than the other private plans. The state may set reimbursement requirements, or require an insurer to target premiums that are a certain percentage cheaper than other plans or its own premiums the previous year. They are even in the same risk-adjustment as other Obamacare plans. It’s like a government sponsored private plan that isn’t capitated like Medicaid Managed Care or Medicare Advantage. Small targets to reduce premiums and lead competitors to do the same via competition are used instead. But that’s the only real difference, the government sponsored targets and sometimes defined design. Otherwise, these plans are sold along with other Obamacare plans and compete with them.

In Washington state, the government contracts with a private provider that must set the reimbursement rate for this plan at about 160% of Medicare rates, knowing that private providers in the state were reimbursing around 174% of Medicare rates on average. They must sell plans at multiple metal levels. They thought it would be 5%-10% cheaper than most plans, but the silver “public option” was 11% higher than the lowest cost silver plan in 2021. As a result, only 1% of individual market shoppers chose these plans in 2021.

In Colorado, the “public options” must follow strict design, pricing, and transparency regulations with an annual target to reduce their own premiums by 15% from 2021 levels, or about 5% a year for three years starting in 2023. If these sponsored plans fail to meet their target, then the state will investigate if they must set reimbursement rates. About 13% of individual market enrollees chose one of these options in the first year, but 90% of these plans failed to meet their pricing benchmark. Part of the issue may be the plan design. If the plan design is too generous, that makes it difficult to lower prices for these plans over time, let along for non-sponsored plans in the marketplace.

In Nevada, the state is working to launch a similar series of “public options” by 2026. This set up requires insurers that hold Medicaid Managed Care contracts with the state to bid for a plan on the state’s individual marketplace that target premium reductions of 10%-20% each year to lower the uninsured rate. However, projections only anticipate this scheme lowering the uninsured rate in Nevada by 4,800 people at most when the uninsured rate is 350,000. Perhaps this option will do more to save money for the state and enrollees than expand coverage, but only time will tell.

PBMs and more

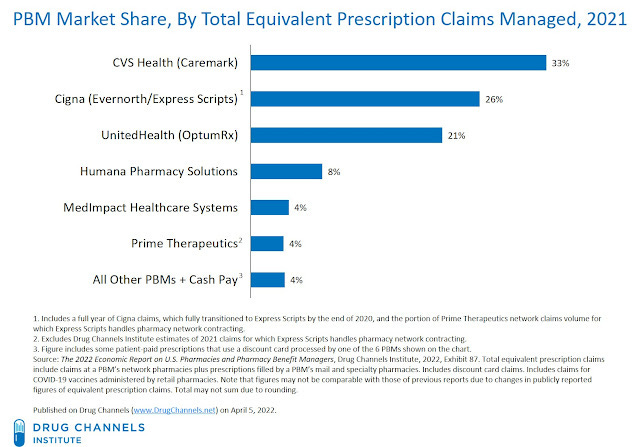

Pharmacy benefit managers (PBMs) are the “middle men” that manage drug benefits for health insurers. These are both private and less regulated than true health insurance. The top three PBMs control 80% of the market, and are owned by CVS, Cigna, and UnitedHealth Group. These operate as private managers for prescription drug benefits even to regulated and subsidized health insurance plans.

If the insurance markets in Medicare, Medicaid, employer insurance, Obamacare, and government sponsored options isn’t enough, many companies will go into provision of care itself. UnitedHealth Group owns the insurer UnitedHealthcare, the PBM OptumRx, the health savings accounts in OptumBank, the healthcare IT and services in OptumServe, and the providers and more within OptumHealth. CVS owns it’s pharmacies, the PBM CVS Health, and the insurer Aetna. And many companies cross between provision and insurance models, like UPMC. At every step of the process in these major national programs, the private sector plays a substantial role. Even policies that would expand access to Medicaid, Basic Health Plans, and Medicare are likely to increase coverage via private insurance, often more than what you would consider “public” government insurance. Medicare, Medicaid, employer insurance, or Obamacare; it’s all Blue Cross Blue Shield.

And what about the socialized medicine system within the Veteran’s Health Administration? Even the VA and Tricare have third party administration from companies like Optum and regional management by private providers.

Does This Distinction Matter?

If Medicaid is anywhere from 10% to 28% purely public, Medicare is at most only half purely public and less if you consider Part D or Medigap (let alone Part A and Part B contractors), employer insurance and Obamacare are privately run, and even state public options and Basic Health Plans are privately run, where does that leave the discourse over public insurance vs private insurance? Is it about pure government provision and logistics? Then maybe only the Veteran’s Health Administration, Indian Health Service, and pieces of Medicaid qualify. Is it about government subsidy, government control of prices, and strict regulations? Then maybe Medicare, Medicaid, and Basic Health Plans qualify, including private Medicare Advantage and Medicaid Managed Care Organizations. Is capitation the only way to allow for price controls, or do indirect price controls like strict targets work? Then maybe state public options qualify as well. Are price controls all that matter? That can’t be the case, because Medicare and Medicaid didn’t have their proper price setting until the 1980s.

More likely, the debate of public versus private is a spectrum rather than a hard cut off. Our programs for military families and natives are entirely socialized, Medicare and traditional Medicaid are mostly public with some private involvement in payment, Medicare Advantage and Medicaid Managed Care are publicly provisioned privately outsourced for a set cost, and Obamacare and Basic Health Plans are publicly provisioned privately outsourced for an uncapped cost regardless of other measures to cut costs. With employer plans the being the largest scheme with the least oversight, and funding via exemption of taxes on the money employers spend to care for their employees.

Do state public option plans count as public insurance, and does it matter? In our current healthcare system, is this distinction helpful? It is the public vs private dichotomy between Medicaid/Medicare and Obamacare even meaningful? Is the ultimate goal to increase the scope and breadth of public insurance, or is it to grant access to as many people as possible at a price people are willing to pay? Maybe the better question is: do these plans provide decent coverage and bend the cost curve? And what are the most effective ways for us to bend the cost curve? Capitation, premium targets, bundled payments and global budgets, wellness programs, or direct price setting? These can all be done successfully or neglected with government insurance or private insurance. They can be managed competently or incompetently. Though anyone can express a preference, public or private provision is the agent for the means to an end. Not an end in itself. Maybe the focus should be primarily on how to make the best functioning system that is possible, and improve it as best you can. Not just focusing on the labels of public vs private, or the state vs the market. Especially since they are they are all managed by private providers regardless.

And finally, at what point are we putting too much weight on our healthcare system and not enough on other welfare programs? Should the focus being on the absolute highest quality of care for the cheapest price, or would our welfare state be better served (and healthcare costs lower) with more effective provision of affordable and plentiful housing, healthy food, a good education, and a stable income for American families? Not only would further spending in these areas reduce poverty, but the reduction of poverty very well could lead to fewer instances of disease and more affordable healthcare for everyone.

Thanks for an excellent summary.

I have an article I would like you to review, but I do not know how to reach you. Maybe send me an email at bob.hertz@frontiernet.net. thanks