Some of the Ways We (Try) to Control Health Care Costs

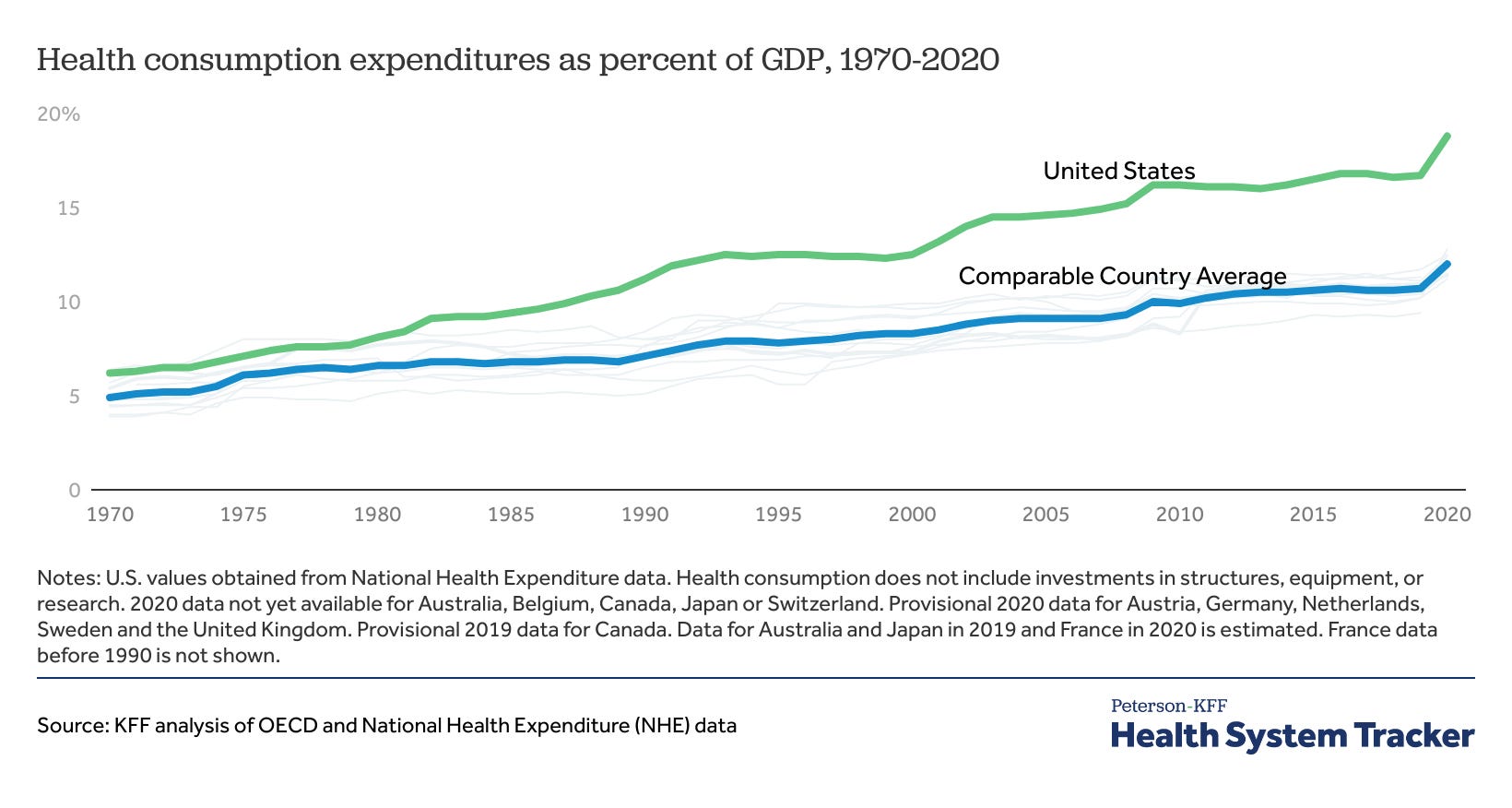

Health care in the United States, it’s very expensive. About 18% of our Gross Domestic Product is spent on health care, much more than any other developed country. This is despite lacking universal health coverage. We know that private insurance spends far more than public insurance like Medicare per procedure, but how do we try to control health care spending? In this post, I’ll review a non-exhaustive list of some of the ways.

Changing Behavior

If you want to lower costs, you can encourage people to engage in healthier behavior. So, governments and employers try to find ways to do just that.

Wellness Programs

About half of people in the United States are covered by employers for their health insurance, and most of them are in completely self-funded health plans. Employers get broad discretion for how to determine their coverage, they just have to meet minimum requirements covering 60% of costs on average along with free preventative care.

In order to keep their costs down without reducing coverage, employers may resort to wellness programs. They could pay for gym memberships or have gyms on site, conduct voluntary health surveys to nudge people to think about their health more, encourage people to exercise, have free biometric screenings, and more. For employers with Health Savings Account (HSA) eligible plans, they may even offer to contribute towards their employees’ HSAs or reduce their premiums if the employee engages in these activities. But do these programs actually work? Signs point to no. In a randomized experiment, employees at participating sites had no different results compared to their control group across 27 different measures of health. And that’s in a randomized experiment. In completely voluntary set ups, participants tend to be employees that were already health conscious. Effectively, this could lead to de facto underwriting without any of the benefits of bending the cost curve.

Externality or “Sin” Taxes

Externality or “Sin” Taxes are aimed at disincentivizing behaviors that could bear a cost on society that the consumers don’t fully bear on their own. The idea is to make the people involved in the behavior leading to higher costs bear more of the burden; often to reduce that behavior and make them internalize the cost. Some examples are alcohol taxes, tobacco taxes, and sugar taxes. Rather than banning the behavior, the government can tax it. They can even use the money to help pay for the costs of the behavior like through reinsurance on expensive claims, awareness campaigns, funding for health departments, etc.

The general finding is that for a 1% increase in the price of alcohol or tobacco, there is a corresponding 0.5% decrease in sales. Though it’s an expensive way to reduce spending by consumers, the research seems to say that it works. However, while some governments say they will use the revenue to address the problem directly, that’s not always the case. Sin taxes can be a way for governments to make an easy dollar without further addressing the problem.

Coding and Pricing Methods

Other than changing behaviors, we can control costs by negotiating on the pricing directly.

Diagnosis Related Group Codes

In the 1950s and 1960s, insurance companies and the government used to pay for a simple accounting of the costs billed to them by the hospital or provider. However, paying this amount without asking further questions encouraged providers to charge whatever costs the insurance companies and patients could bear. As a result, medical inflation was out of control and government spending grew quickly each year for programs like Medicare and Medicaid. In 1983, the government switched Medicare to a Diagnosis Related Group (DRG) system. This created a flat fee that Medicare would pay for a given procedure based on severity and several other factors. In Medicare’s Inpatient Prospective Payment System, payments are also adjusted for regional labor and capital costs, the DRG, and other factors like Disproportionate Share Hospital Payments for hospitals that handle a larger proportion of the uninsured and Medicaid patients. Private insurance and Medicaid picked up their own systems of coding and usage of these codes is commonplace today.

Naturally, reducing what providers are paid for a procedure could mean they make less revenue per procedure, so they may try to increase patient volume, increase the number of procedures, and discharge patients as quickly as possible to get as much revenue as possible. In a fee-for-service system where providers are paid by service, this is exactly what can and has happened.

Managed Care and Capitation

To avoid the incentives for increased volume in fee-for-service, insurance companies and governments have shifted to managed care and capitated models. In Medicaid Managed Care Organizations, these organizations are given set per enrollee payments each month to cover the costs of care and they must work within their budget to address patient needs. Types of Health Maintenance Organizations and other models may use this strategy as well. Of course, patient needs vary, so the overall risk of a population is accounted for when determining payments. But just like drawbacks with other insurance models, this pressure to keep costs down may result in narrower networks of providers, gatekeepers to prevent overutilization by patients, prior authorization of a procedure, denials of care, or even government contractors exaggerating to the government about their population’s complexity to increase their payments.

Medicaid Managed Care has failed to achieve further cost savings, costing slightly more with similar goals. This may be because government spending on Medicaid was already quite price sensitive, so allowing for for-profit overhead just made things worse.

Health Maintenance Organizations have successfully lowered health care costs for their enrollees when compared to indemnity insurance. Partly by having healthier enrollees in the first place, but also by paying less per procedure and selecting providers that will accept those cheaper prices into their network. Similar insurance models like Preferred Provider Organizations, Exclusive Provider Organizations, and Point of Service Plans achieve similar results to a lesser extent.

Patient-facing Costs

Another way you can get someone to appreciate the costs of care and act accordingly is to have them bear some of the burdens of the costs when choosing to get care. We have no shortage of ways to do that in the USA.

Typical Cost sharing

In any given insurance plan, you are likely to have deductibles, copays, and coinsurance. Copays are flat fees for a given visit. Deductibles set the amount at which your insurance will begin to help, before that your care is at your cost. Afterwards, coinsurance may kick in where you still must bear a smaller share of the total cost of a procedure. The benefit of this is that a patient may think twice before going to the doctor if they know it could cost them a lot of money. The downside is they may avoid necessary care for their health. And patients aren’t very good at knowing the difference. Furthermore, this is rationing care by ability to pay, so wealthier people are less likely to skip care while sicker and poorer patients may continue to avoid treatment.

Health Savings Accounts and Flexible Spending Accounts

HSAs and Flexible Spending Accounts (FSAs) are tax-free accounts you can use to pay for medical expenses. For HSAs, you can save a given amount that rolls over each year and invest the rest, but you need a high deductible health plan to get access. FSAs don’t have that requirement, but only allow you to contribute a small amount towards it and any unused money at the end of the year is lost.

These can be used to increase your deductible so you have to bear the costs of care for longer, while also encouraging saving for the care. But the benefits of HSAs are almost entirely received by the top 5% of earners, and many people skip care more often as a result.

Reference Pricing

Coinsurance gives patients rewards for shopping for cheaper care than copays do, but many aspects of health care pricing aren’t transparent and aren’t shoppable. You may lack the knowledge of costs or you may not have the ability to shop, like in an emergency. But that may not be true for things like prescription drugs or elective procedures. The problem is most prescription drug plans operate on flat copays that make no difference to the patient which drug they get. Copays may be tiered based on the preference of pharmacy benefit managers, but that does not mean the actual cost is less for the drug with the smaller copay. Reference pricing addresses this by setting a share of coverage for the patient on a given procedure based on a preferred provider that is likely quite cheap. If patients want to go to a different provider that is more expensive, they pay the difference. This has potential to reduce health care spending, but may not work if paired with an out-of-pocket maximum. And on the other side, not having an out-of-pocket limit could be devastating to the sickest patients.

Beyond Fee-For-Service

As I said, fee-for-service incentivizes volume over quality of care. In recent decades and especially with the passage of the Affordable Care Act in 2010, the government and insurance companies have been experimenting with various versions of value-based care.

Pay for Performance

Rather than paying for each performance alone, the Centers for Medicare and Medicaid Services (CMS) has been utilizing Pay for Performance Models (P4P). This involves reviewing quality of care outcomes, readmissions rates, complications, etc. If hospitals meet a quality-of-care benchmark, they can earn bonus payments. In some value-based programs, CMS uses a small across the board cut to reimbursement rates and offers providers a chance to earn back a portion of the funding if they meet said benchmarks. These programs can save Medicare hundreds of millions of dollars per year.

Bundled Payments

Because DRG payment systems pay by the code, providers may still increase revenue by coding procedures as medically complex as possible and finding as many things to code as possible. To prevent this, paying for an entire “episode of care” by a per episode bundle can save the government or insurance companies some money. For example, CMS has programs like Bundled Payment for Care Improvement (BPCI) and Comprehensive Care for Joint Replacement (CJR). For CJR, hospitals are given a target price to meet in a 90-day episode of care based on recent regional prices. If hospitals meet the target price and stay within their quality goals, then they can earn a reconciliation payment to share their savings with Medicare. Rather than costs being tied to each procedure, it’s tied to the procedure, readmissions, post-acute care, and any complications that may result during the episode. Hospitals can even enter gain-sharing agreements with post-acute care providers, so providers are incentivized to coordinate care. On the other end, hospitals can be penalized for failing to meet target pricing or quality of care goals.

Just like with DRGs, this causes rationing of care to reduce spending, albeit in a more complex way. However, creating these target prices could mean that hospitals would save money by avoiding the more complicated patients, or cutting back on necessary care just like DRGs can. Careful review of these models is necessary to avoid harming the most vulnerable patients.

Accountable Care Organizations

Accountable Care Organizations (ACOs) were created by the Affordable Care Act to save the government money on Medicare by coordinating care. Networks of providers that agree to participate can get a set budget per patient in a population, like say Medicare patients with end-stage renal disease. If they meet quality of care and annual spending benchmarks, they can share the savings with Medicare just like bundled payment models. The difference being that ACOs focus on annual spending rather than per episode spending. Comparisons to HMOs have also been made, but ACOs are voluntary and not an insurance model. Furthermore, patients can leave the model in certain circumstances. ACOs also do not have a hard capitated limit, and instead rely on sharing gains and losses with Medicare.

Though bundled payments and ACOs are primarily conducted in Medicare, private insurance companies have also been experimenting with them in employer insurance and Medicare Advantage.

All-Payer and Global Budgeting

One of the most comprehensive programs to address health care costs is Maryland’s Total Cost of Care Model. This program combines the Maryland Primary Care Program to coordinate care, Care Redesign to improve quality of care, and Maryland’s All Payer Model.

For decades, Maryland has set prices per hospital for all procedures regardless of insurance type. So, Medicare, Medicaid, CHIP, Obamacare, and any employer plan all paid the same price for the same procedure. That made things less expensive for private plans, but holes existed in the outpatient setting and with traditional fee-for-service set ups. In recent years, the model has included the outpatient setting so hospitals can’t just discharge patients quickly to avoid price setting. Additionally, Maryland included a global budget per hospital much like ACOs or capitation to solve the problem of overutilization. The expanded version of the model is new, but the results are promising. In 2019, Maryland reduced total cost of care spending by $365 million, even more than before the introduction of the global budget or the inclusion of the outpatient setting. As a result, unsubsidized premiums on the individual marketplace are the cheapest in the country.

Conclusion

There are no shortage of ways we try to control costs, though the results are inconsistent. And some of the more effective methods are not without their own tradeoffs. By setting prices too low on a procedure, hospitals may increase volume to make up the revenue. By capitating payments, networks may narrow or patients may go without care. Cost sharing is a blunt tool that leads to avoided unnecessary and necessary care. And bundled payments and global budgets may lead to providers turn away more complex patients, the people most in need of care. Wherever you look, the system is littered with tradeoffs. So far, we have chosen dozens of small experiments split between the government and private insurance rather than a single comprehensive approach like Canada’s single payer, the United Kingdom’s National Health Service, or Germany’s and Switzerland’s rate setting (though Maryland does this). Until we are committed to facing the tradeoffs, health care costs will remain high.

Great article, thanks for sharing!