Choice overload and the Affordable Care Act

The Biden Administration’s half-step towards easing enrollment by limiting insurer offers

The Affordable Care Act (ACA) individual health insurance marketplaces are where households can shop for qualified health plans and receive premium tax credits to help pay for these plans. Healthcare.gov, or the federally facilitated marketplace (FFM), is a tool for shoppers to compare qualified health plans which are sorted into four metal levels that contain all “essential health benefits.” Since President Biden took office, ACA enrollment has increased to 16.3 million; 12.2 million of which is on the FFM. And enrollment is not the only thing that has increased recently, plan options have increased substantially as well. In 2023, 92% of enrollees have three or more qualified health plan (QHP) issuers to choose from. In 2019, enrollees had an average of 2.8 QHP issuers; in 2023, 6.6 insurers offering plans. In 2019, shoppers had an average of 26 different health plans to choose from; now in 2023, shoppers are overwhelmed with an average of 113.7 plans to choose from. With so many options along such a wide range of coverage quality, too much choice can be overwhelming and lead to people putting off plan selection or selecting a dominated or suboptimal choice.

On December 12, 2022, the Biden Administration published a proposed Notice of Benefit and Payment Parameters (NBPP-2024) for 2024 governing the ACA marketplaces. In the NBPP-2024, the Administration aims to simplify plan choice by limiting the number of plans offered via one of two methods: limiting insurers to two non-standardized plans in each metal tier and network category, or creating a “meaningful difference” standard that will limit insurers to plan offers with deductibles at least $1,000 apart. However on April 17, 2023, CMS released their final rule in which they chose a different path. Four non-standardized plans were allowed in each metal tier and network category. In what follows, we will explain how these different policies could have affected the number of choices offered in the ACA marketplaces, and how much the policy in the final rule could as well.

Standardization and past NBPPs

Plan standardization is not a new concept to health insurers that offer plans on the FFM. In the 2017 NBPP, the Obama Administration made it optional for insurers to offer standardized bronze, silver, and gold plans based on the most popular plans in previous years. These choices were differentially and preferentially displayed as “simple choice” plans in 2018. The Trump Administration proposed to eliminate these standardized plans, but the rule change was held up by the courts. Plan choice counts substantially increased after 2019. In July 2021, President Biden issued an executive order directing the Department of Health and Human Services (HHS) to review further ways to standardize plans and simplify enrollment.

In the 2023 NBPP, HHS required insurers offering plans on Healthcare.gov to offer standardized plans in the 2023 plan year. This rule does not apply in states that operate their own marketplaces although several already standardize plans. Health insurers offering health plans on Healthcare.gov must offer a standardized plan for every plan-network type (HMO, PPO, POS, EPO), metal level, and region where they compete. These standardized plans will be based on the most popular QHPs in the 2021 plan year. HHS did not limit the number of non-standardized plans in the 2023 NBPP or create a “meaningful difference” standard in order to have more time to study the costs and benefits of plan choice space modifications. However, for the 2024 plan year it appears they are ready to move forward.

The Proposed 2024 NBPP Rule Change and Possible Effects

As we explained above, the Biden Administration proposed limiting the number of plan choices via two possible changes: 1) limiting QHP issuers to 2 non-standardized plans for each metal tier and network type, and 2) creating a “meaningful difference” standard that will require health plan deductibles to have a difference greater than $1,000 compared to other plans offered by a given QHP issuer at a given metal level and network type. Like the 2023 NBPP, these rules will apply to all QHP issuers on Healthcare.gov. However, these changes would not have applied to catastrophic plans and standardized plans will no longer be required for non-expanded bronze plans. The first part of the proposed rule change would thus have limited issuers to two non-standard gold per plan-network type. If a single insurer offers both an HMO and a PPO in a county, that insurer could offer two standard gold plans and four non-standardized gold plans.

The second option of this rule would have allowed for unlimited plan variation within a metal level and plan-network type as long as each plan has a deductible that differs by at least $1,000 from any other plan in the same metal level and plan-network category. Pragmatically, this is a limit of ten plans per metal level and plan-network dyad.

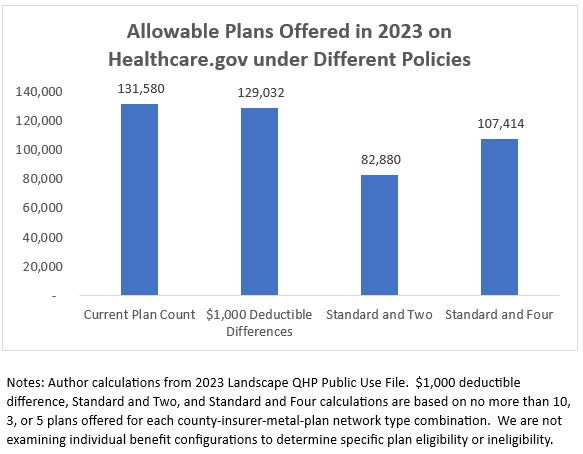

How would each affect the number of plans offered in the ACA marketplaces? Using the 2023 Landscape Public Use File, we counted the number of plans in each county offered by each insurer-plan network type-metal level triad. We then compared them to the number of allowable total plans under both proposals in order to see how these rules could reduce offerings. This will establish an upper limit of the number of plan choices in each rule, rather than projecting the real effects of these policy options. If issuers do not take advantage of all their choices, plan option will necessarily be lower than presented. For these 33 states, a total of 131,580 plans were offered across all metal levels for plan year 2023. This ranges from a high of 12,388 in Texas to a low of 87 in Delaware.

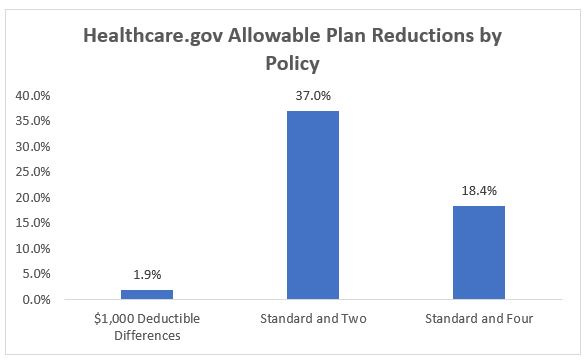

Under our estimates, we believe that the “meaningful difference” standard would have only reduced nationwide choices on Healthcare.gov to 129,032, or a reduction in allowable plan choice of only 1.9%. In 19 states, this will have no effect on allowable plans slots at all. However, limiting issuers to two non-standardized plans would have reduced the number of allowable plans nationwide to 82,880, or by 37%. Under CMS’s Final Rule of limiting issuers to four non-standardized plans, allowable slots could be reduced to 107,414; an 18.4% reduction. All states other than Alaska would have been affected in some way by the two non-standardized plans limit. As is to be expected, Bronze plans, with their high deductibles, are almost entirely unaffected by either of these potential rule changes. Under the “meaningful difference” standard, Expanded Bronze and Silver plans would have had modest changes to the number of allowable offers, while Gold plans would have had few changes to allowable offers. Under the two non-standardized limit standard, allowable Expanded Bronze and Silver plan offers would have been greatly affected in some states with Gold plans affected to a lesser, but noticeable, extent. In some states, the number of allowable Expanded Bronze and Silver offers could have been cut roughly in half. The actual policy passed, the limit of four non-standard allowable plans, is a watered-down version to the two non-standard plan policy with similar possible effects to a lesser extent.

Reviewing this in terms of a typical issuer, these results are even more revealing. Counties in states that use Healthcare.gov have an average of about 4.01 QHPs per issuer to choose from in a given metal tier. The “meaningful difference” deductible rule would have reduced this to 3.93 QHPs per issuer, while the limit of 2 non-standard QHPs for would have limited counties to an average of 2.52 QHPs per issuer in a given metal tier. The finalized rule of four non-standard plans could set an average of 3.27 QHPs per issuer. Therefore, a county with four issuers competing for Bronze, Expanded Bronze, Silver, and Gold plans may expect their number of plans to choose from to decrease from 64.2 QHPs to a maximum allowed amount of 62.9 QHPs under the “meaningful difference” rule, 40.3 QHPs in the 2 non-standard plans rule, and 52.3 QHPs in the final rule allowing four non-standardized plans. This, of course, does not account for variation in dental or vision plans.

Limiting issuers to two non-standardized offers could have meaningfully reduced total plan offers for insurers that offer multiple plan types and across all metal tiers. Reducing the number of plans offered in this way could have limited the diversity of plans within a metal tier, but also simplified comparisons for shoppers. Watering down this proposal to four standardized plans could have an effect not as widely felt by consumers and its ability to prevent choice overload will be limited. CMS estimates that its chosen policy will reduce the average number of plans for consumers from about 113.7 plans in 2023 to about 90.5 plans in 2024, or about a 20% reduction in the number of plans. Building on this policy with further tailoring in the future could be promising. It could be weak tea, or it could be the start of making choices far simpler for shoppers. Only time will tell.

P.S. Special thanks to David Anderson, health policy writer with his own blog Balloon Juice, for involving me in this analysis of NBPP-2024.